CAREFUL CASH FLOW DUE TO COVID

Managing your cash flow has become critical since this Covid crisis emerged. Most have lost or have reduced income. To meet this historic challenge the governments have legislated emergency financial assistance for those unemployed after the business stoppage. Before requesting an early distribution from your retirement savings or using financial support for continuing expenditures as usual, it is a time to look at your spending patterns and habits.

Zero-based budgeting is a good discipline. Scrutinize each item for whether it is critical. Some items can be reduced, others postponed. Much of daily spending can be habitual or add-ons at the check-out. If already faced with debt or mortgage payments, it maybe that a moratorium could be arranged or a restructuring of the debt altogether. A good benchmark is that debt payments should not be more than 1/3rd of gross income, preferable less. This is known as the debt-to-income ratio (DTI). For example, income of $5000 a month should have monthly debt payments of $1,500 or less. For an overview of cash flow, construct an income statement that captures all income and all expenses. The difference is your net cash flow. If it is negative, changes are in order. Extra funding may come from savings or by receiving emergency funding.

The balances of savings accounts and pensions will be reported on a Balance Sheet which ‘balances’ assets and liabilities. A balance sheet lists the total current value of the monies, investments, and pensions, along with amounts to be received, as well as houses, boats, cars or other valuables which are known as assets. The balance sheet also lists the total balance owed on loans, mortgages, or other financial commitments. These are the liabilities. The difference is Net Worth or Equity for companies. A debt ratio of assets divided by debt indicates whether debt is at sustainable levels. It should be in the range of 0.6 - 0.7, ie $500,000 debts/$350,000= 0.70 debt ratio. More than that can be troublesome. This is one of the reasons to be careful about drawing from pensions. It will dwindle the asset side of the equation. There are promotions encouraging pension withdrawals to put the funds in another account or to invest in something less secure. Think twice.

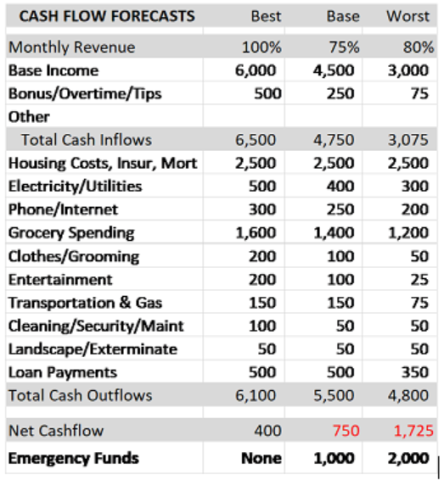

There are so many unknowns about when and how business will resume, and what will be the income or revenue received. Plan for more than today. It is difficult to get an accurate idea of how long any shortfalls will need to be funded or what they may be. In this case, it is useful to make three cashflow forecasts or scenarios. One scenario is the best case, where the lost revenue is minimal if at all. The base case is based on known information and the spending cuts that need to be made. The worst case is where things go on for longer which will necessitate more cut-backs and work-outs. In the worst-case scenario, all the difficult choices can be considered in order to prepare accordingly. The following format can be used and adapted for business use.

These scenarios will provide a planning picture. The amount of emergency funds needed will be estimated by the number of months in the various scenarios. A basic financial planning guideline is to have three months of spending in an emergency account when there are two incomes in the household. In a one income household there should be a six-month emergency fund. It is a good idea, but difficult to achieve without planning for it. Put monies in a different account so it is not co-mingled with the normal operating account. If drawing it down now, remember to replenish it when possible. In the other event, if things stay bad for longer, major rethinking of expenses and possibly housing will be in order. Bulk-buying or house-sharing could address the two large expenditures. Another idea is to look at other means to raise income by making something to sell or offering services that can be done independently. There are also boot sales and emoo. Difficult times take difficult measures.

There are a number of services to assist people and business with cashflow forecasts. Financial Services has a form to assess financial status. The SBA has a offered assistance for their support. Many of the pension services have templates to determine current and retirement cashflows. This points to the fact that it is important to think long-term. Really long-term. Balance actions today with what will needed in the future. Financial planners such as Senior Solutions Ltd can guides client by quantifying cash-flows and cash goals in the future. What can be funded through savings and investment approaches and what might need to be reined in? Those are the questions. Check out savings patterns to cash goals to see if the goals can be met. SeniorSolutionsBDA.com has a MAKE a PLAN button on the upper right of the landing page for specific goal funding. Or send a request to SeniorSolutionsBDA@outlook.com for a cashflow forecasting worksheet.

Patrice Horner, Director of Senior Solutions Ltd (SSL), holds an MBA in Finance and is a Certified Financial Planner (CFP-US). SSL provides financial planning guidance for a fee. The client receives guidance to implement at their own discretion. SSL does not guarantee any returns from such guidance. SSL is not an investment manager, does not sell investment or insurance products, nor receives any commission or third-party compensation. SSL does not directly manage or custody assets on behalf of clients. SSL is a financial planning firm for select clients.